总:海上鲜作为一站式渔业综合服务企业,递交港交所上市申请,2023年营收超9亿元,有望成为“中国内地数字渔业第一股”。

1. 业务涵盖海鲜销售、燃油销售、供应链管理、海上通信及IT解决方案等,通过HSX App高效链接上下游,覆盖宁波及多个沿海城市如防城港、烟台港。

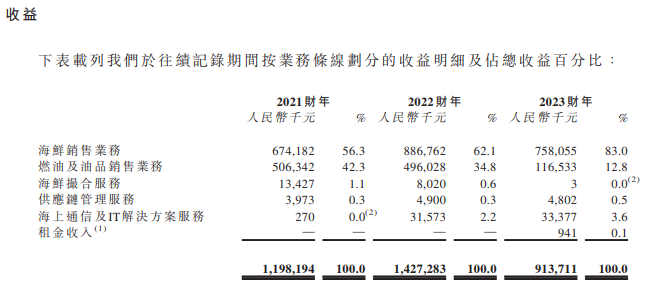

2. 2023财年营收9.14亿元,毛利率7.9%,海鲜销售贡献83.0%收入(毛利率2.4%),燃油销售占12.8%(毛利率20.3%),年内溢利3580.3万元。

3. 自2015年成立以来,完成6轮融资,累计募集4.04亿元,投资方包括北斗星通、顺为资本等十余家机构;IPO募资拟用于数字渔港项目、扩展销售网络(深圳和成都新办事处)、收购机会及偿还借款。

总:海上鲜的业务模式展示数字渔业在品牌渠道建设和消费趋势中的应用,海鲜销售主导收入反映用户需求。

1. 品牌渠道覆盖多个沿海城市如宁波象山港、福建福州港,提供扩展机会;使用HSX App链接上下游,提升交易效率,体现数字化渠道建设。

2. 海鲜销售业务2023年占营收83.0%,毛利率2.4%,燃油销售毛利率20.3%,数据提示定价策略和价格竞争空间;消费趋势显示海鲜需求稳定增长。

3. 一站式服务包括供应链管理和海上通信,启示产品研发方向,如结合北斗技术提升渔业服务;市场份额小(海鲜0.2%),凸显品牌差异化机会。

总:海上鲜的上市和业务扩展提供增长市场机会,财务数据变化提示风险与可学习点。

1. IPO募资用于扩展销售网络(深圳和成都新办事处)、寻求收购及投资机会,显示增长策略和合作方式;消费需求层面海鲜销售占主导,2023年收入7.58亿元。

2. 年内溢利波动(2021年4534.2万元、2022年3412.3万元、2023年3580.3万元)和毛利率变化(5.5%到7.9%)提示成本控制风险;海鲜销售业务增长快(2022年8.87亿元),机会提示可学习数字化撮合模式。

3. 最新商业模式如一站式综合服务,包括供应链管理解决融资难题,扶持政策通过IPO增强;事件应对如扩展网络应对区域覆盖不足。

总:海上鲜的供应链服务和数字化基础为工厂提供产品生产启示和商业机会。

1. 供应链管理服务解决渔业经营者融资难题,启示产品生产和设计需求,如结合数字渔业优化供应链;覆盖宁波—舟山港及多个沿海城市,提供区域性商业机会。

2. 业务以“北斗+互联网+渔业”为基底,推进数字化和电商启示,如海上通信服务提供Wi-Fi设备安装,提升生产环节通信效率。

3. 海鲜销售业务占营收高比例(2023年83.0%),显示工厂可关注海鲜加工合作;IPO募资用于数字渔港项目,启示工厂参与数字化升级机会。

总:海上鲜整合新技术解决渔业行业痛点,提供行业发展趋势和解决方案参考。

1. 行业发展趋势:数字渔业服务模式(如海鲜撮合、供应链管理)2022年市场份额小(海鲜0.2%,燃油0.3%),有巨大发展空间;新技术包括北斗定位与互联网结合,提升服务效率。

2. 客户痛点解决:海上通信服务提供Wi-Fi设备安装,解决渔民海上通信难题;IT解决方案支持HSX App链接上下游,应对交易效率痛点。

3. 解决方案示例:供应链管理服务为中小企业融资提供支持;燃油销售业务毛利率波动(2021年8.0%到2023年20.3%)提示服务商优化方案需灵活。

总:海上鲜的HSX App平台模式体现商业对平台的需求,IPO计划涉及平台最新做法和招商。

1. 平台最新做法:通过App高效链接海鲜交易上下游,覆盖宁波及多个沿海城市;运营管理包括扩展销售网络(深圳和成都新办事处)和寻求收购机会。

2. 商业需求与问题:平台需解决区域覆盖不足(辐射至防城港等港口);IPO募资用于奉化数字渔港项目,涉及平台招商和运营增强。

3. 风向规避:财务数据如年内溢利波动提示风险控制;海鲜销售主导收入(83.0%),平台可聚焦高增长服务;供应链管理服务提供融资解决方案,规避交易风险。

总:海上鲜的商业模式提供产业新动向研究案例,包括市场份额和融资数据启示政策法规建议。

1. 产业新动向:一站式数字渔业服务模式(海鲜销售、燃油销售、供应链管理等)创新结合北斗+互联网;2023年海鲜销售收入7.58亿元占83.0%,显示产业整合趋势。

2. 新问题与政策启示:市场份额小(海鲜0.2%,燃油0.3%)提示竞争格局问题;融资历史(6轮累计4.04亿元)和IPO计划反映政策支持需求,如数字渔业法规完善。

3. 商业模式研究:供应链管理解决融资难题,提供企业启示;财务数据如毛利率变化(5.5%到7.9%)可用于分析成本结构;覆盖区域广,启示区域经济发展模式。

返回默认