当前中国硬件科技股经过一轮大幅上涨,正站在业绩验证的十字路口,普通读者可理清当前市场核心逻辑,明确参与注意事项。

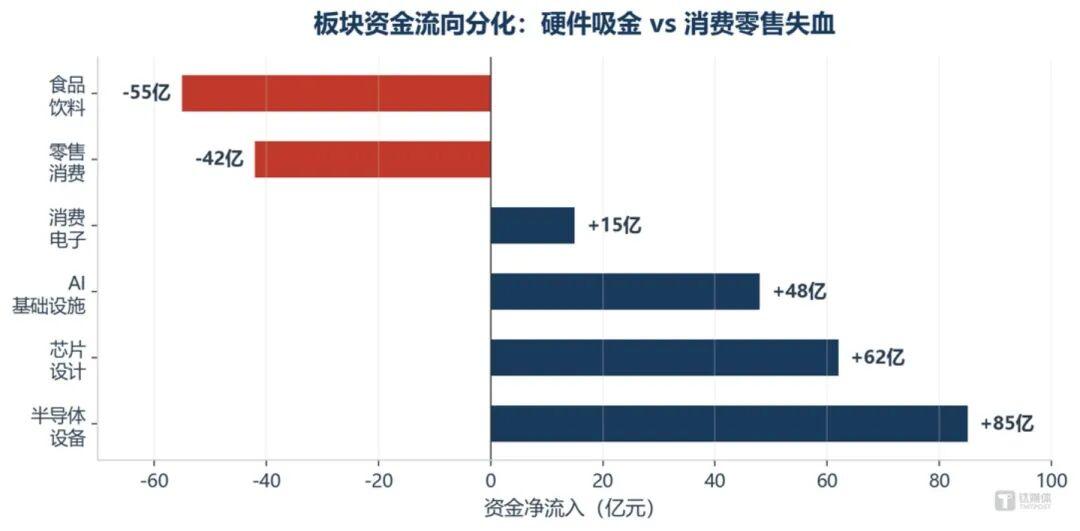

1. 行情基本情况:截至2026年6月26日,科创50指数本季度上涨约62%,PE-TTM攀升至239倍,处于历史100%分位,资金大量涌入半导体、人工智能基础设施、本土供应链相关硬件股,持续撤离疲弱的消费零售板块。

2. 实操参考:后续硬件股能否持续上涨,核心要看业绩能否兑现,7月即将到来的中报密集披露期是本轮大涨后第一个真正的业绩验金时刻,后续行情会出现明显分化,只有订单充足、毛利改善、经营数据达标的公司能维持涨势,只有概念没有真实业绩的公司会被淘汰,普通参与者要注意甄别,不要盲目追热点。

当前全球AI硬件需求高涨,叠加本土替代政策支持,硬件科技相关品牌可从当前行业趋势中明确发展方向,抓住市场机会。

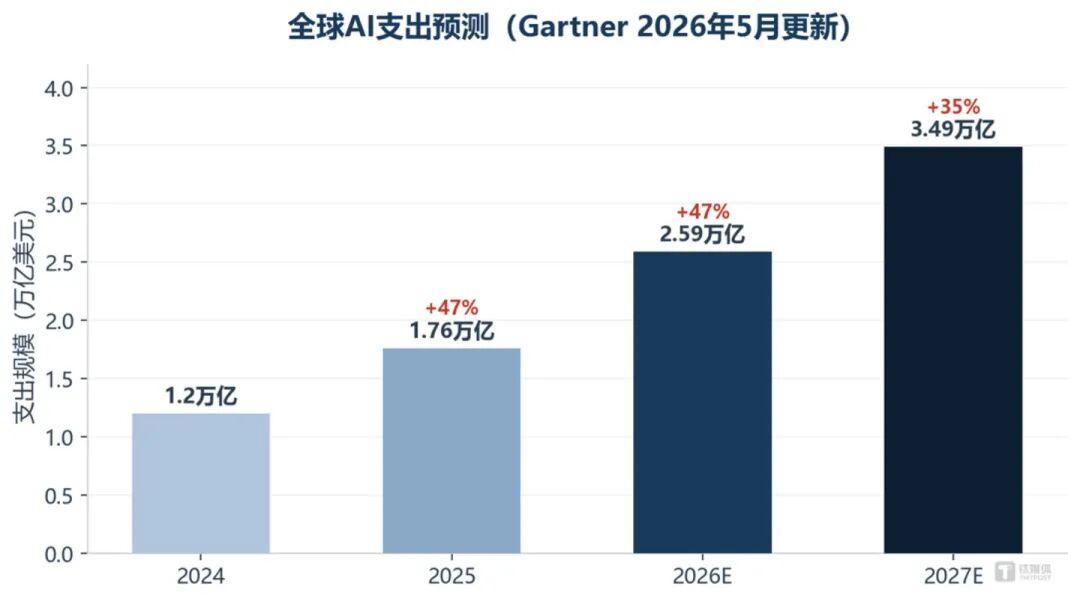

1. 市场需求趋势:全球AI支出持续高增,Gartner将2026年全球AI支出预期上调至2.59万亿美元,同比增长47%,中国AI芯片市场年均复合增长率超过25%,本土AI相关硬件品牌拥有明确的增长空间。

2. 产品研发方向:本土替代和AI硬件是当前核心风口,品牌可参考北方华创“以利润换技术壁垒”的策略,加大14nm/7nm先进制程、先进封装等核心领域的研发投入,巩固长期竞争地位。

3. 结构变化提示:当前资金持续流出消费零售板块,转向硬科技领域,消费类硬件品牌需要及时调整产品布局,贴合AI基建、本土供应链的需求方向。

当前国内硬件科技领域处于政策支持+全球需求拉动的产业周期,硬件相关卖家可从中梳理清晰的机会与风险,提前做好应对。

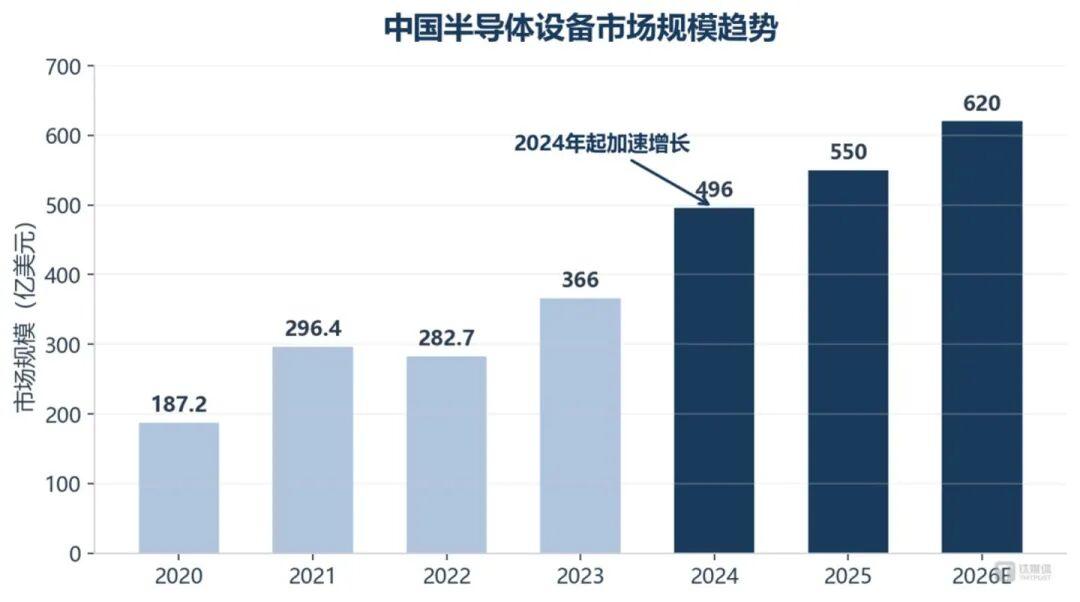

1. 明确增长机会:政策持续支持本土科技龙头,全球AI基础设施建设对芯片及相关硬件维持高需求,本土替代和AI需求双驱动,半导体设备、芯片设计、光电供应、AI基建相关工业硬件都是高增长赛道。当前头部设备企业已经兑现业绩,一季度半导体设备板块营收同比增25.78%,归母净利润同比增60.42%,行业景气度明确。

2. 风险提示与应对:当前板块估值已经处于历史最高位,PE-TTM达239倍,后续行情会大幅分化,只有能兑现真实订单、利润数据的玩家才能留存,只有概念没有实际经营成果的玩家会被淘汰,7月中报就是关键验证节点,卖家要提前梳理经营数据,做好应对准备。

当前全球AI硬件需求爆发叠加本土替代政策推进,硬件生产制造相关工厂迎来明确发展机遇,也需要调整自身方向贴合市场需求。

1. 生产设计需求方向:当前市场核心需求集中在14nm/7nm先进制程设备、先进封装设备、AI相关芯片、配套工业硬件领域,这些领域已经贡献了头部设备企业超65%的新增订单,需求旺盛,工厂可围绕这些方向调整生产和设计布局,贴合市场需求。

2. 商业机会:本土替代已经有扎实的业绩基础,全球芯片需求高增,国内供应商不管是直接参与全球供应还是做本土替代,都有机会分得市场蛋糕。

3. 发展启示:工厂要重视研发投入,舍得短期让利投入技术研发,以此构建长期技术壁垒,同时要关注产能利用率、订单转化率等核心经营指标,尽快把行业风口转化为实际经营成果,避免只有概念没有实际产出。

当前硬件科技行业正处于大涨后的业绩验证阶段,呈现出明确的分化发展趋势,为相关服务商带来了新的业务机会,可针对性调整业务方向。

1. 行业发展趋势:当前行业由本土替代政策和全球AI需求双驱动,整体景气度较高,但估值已经处于历史高位,后续行业分化会不断加剧,不同层级企业的服务需求差异会持续放大。

2. 核心客户痛点:大量中小硬件科技企业当前只有概念支撑,缺乏足够的业绩兑现能力,难以在本轮行情中获得市场和资金认可;而头部企业需要加大研发投入、扩充产能,也需要多方面的配套资源支持。

3. 业务方向参考:服务商可以围绕企业业绩梳理、研发对接、产能优化、投资者关系管理等方向推出针对性解决方案,帮助企业把技术和订单优势转化为清晰的财务成果,更好应对即将到来的业绩验证期,抓住本轮产业周期的红利。

当前中国硬件科技股的行情变化,反映出科技产业发展的新方向,对产业服务、投融资等相关平台来说,需要调整自身布局应对新变化。

1. 市场需求变化:当前市场更偏好直接绑定AI硬件、本土供应链的相关标的,而非泛科技敞口,投资者对业绩真实性的要求大幅提升,平台需要调整招商和标的筛选方向,重点引入有实际订单、研发优势、业绩增长的硬件科技企业。

2. 运营管理调整:当前板块分化趋势明确,平台要加强对入驻标的经营情况的跟踪,及时向投资者提示风险,做好投资者教育,引导市场关注真实业绩而非概念故事。

3. 风险规避:当前整个板块估值已经处于历史最高位,对业绩不及预期的敏感度很高,平台要提前做好风险提示,避免过度炒作概念,防范板块波动带来的相关风险,同时抓住产业周期机会,重点布局优质头部企业打造差异化优势。

当前中国硬件科技股的本轮行情呈现出不同于以往的新特征,为产业研究提供了新的样本,有诸多值得研究的新方向。

1. 产业新动向:本轮行情由政策支持的本土替代和全球AI需求爆发双驱动,不同于过往单纯的情绪驱动行情,资金更偏向贴近实体经济、有真实业绩杠杆的硬件企业,行业集中度提升,领涨集中在半导体设备等少数环节,市场按供应链相关性排序选股的特征明显。

2. 新出现的问题:当前板块估值已经处于历史100%分位,远超当前业绩水平,需要多个季度的业绩持续超预期才能消化估值,且目前只有设备环节兑现了较好业绩,芯片设计等其他环节业绩明显弱于设备环节,整个产业链能否全面跟上需求仍存疑,分化风险凸显。

3. 研究启示:本轮行情验证了政策加真实需求驱动的产业行情比单纯概念炒作更扎实,但同样面临不小的估值压力,参考历史经验,最终能穿越周期的企业不足20%,后续可重点跟踪中报后的业绩验证过程,研究本土硬件企业在全球AI供应链的份额变化,总结本土替代的发展规律。

返回默认