乐歌2024半年报关键业绩亮点

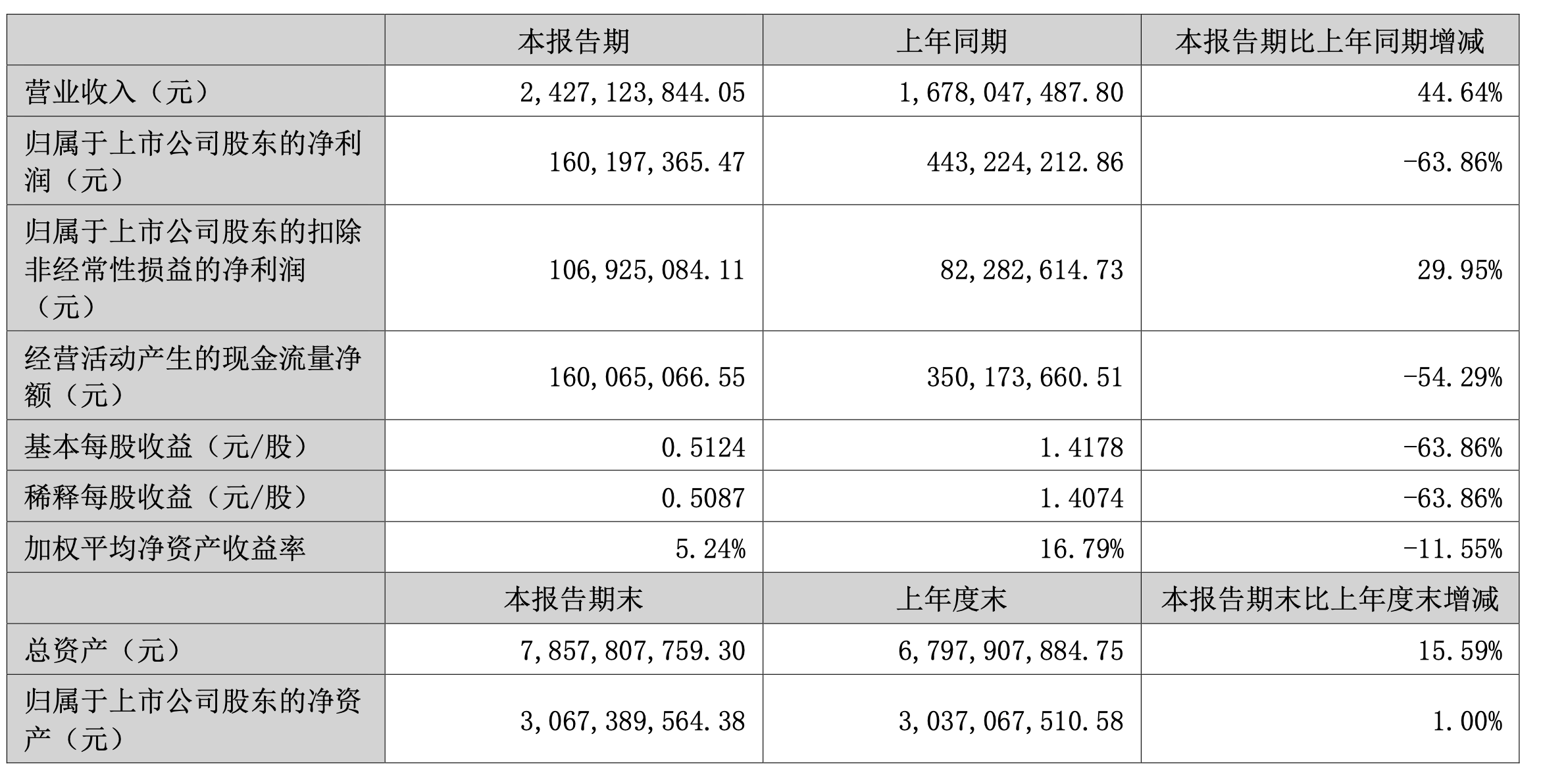

1. 整体营收24.27亿元,同比增长44.64%,显示业务高速扩张。

2. 净利润1.60亿元,同比减少63.86%,主要因2023年出售海外仓的非经常性收入影响;扣非净利润1.07亿元,同比增长29.95%,反映核心业务稳健增长。

产品与渠道干货信息

1. 人体工学系列产品营收13.37亿元,占营收55.07%,是主要收入来源;新品类如电动沙发、人体工学椅销售收入占比约8%,体现产品多元化。

2. 跨境电商收入9.15亿元,同比增长20.36%;独立站收入3.69亿元,同比增长20.87%,占跨境电商收入的40.31%,亚马逊占比53.76%,显示多渠道布局。

海外仓业务实操成果

1. 海外仓营收8.51亿元,同比增长129.88%,毛利率15%,同比提升;全球17个自营海外仓,面积48.21万平方米。

2. 服务778家外贸企业,处理包裹超400万个,同比增长超120%,提供高效物流支持。

品牌战略与渠道建设核心干货

1. 自主品牌产品销售收入占主营业务收入(不含海外仓)68.93%,突显品牌主导地位;新品类销售收入占比约8%,反映产品研发和消费趋势响应。

2. 独立站销售收入3.69亿元,同比增长20.87%,占跨境电商收入40.31%,显示品牌渠道建设成效;亚马逊占比53.76%,对比提供渠道优化参考。

消费趋势与用户行为洞察

1. 人体工学系列产品营收13.37亿元,占比55.07%,结合新品类增长,表明用户对健康办公产品需求稳定;新品类占比提升,暗示用户行为向多元化产品迁移。

2. 海外仓业务高速增长(营收增129.88%),服务企业超778家,反映品牌商可借物流服务提升用户满意度。

增长市场与机会提示干货

1. 整体营收同比增长44.64%,海外仓营收同比增长129.88%,显示跨境电商和物流服务为高增长领域;独立站收入同比增长20.87%,提供可学习渠道模式。

2. 新品类销售收入占比约8%,结合人体工学产品主导,提示消费需求变化机会,如电动沙发等新品开发。

事件应对与商业模式启示

1. 净利润下降因非经常性收入,但扣非净利润增长29.95%,提示风险规避需关注核心业务;海外仓服务778家企业,处理包裹增超120%,提供合作机会。

2. 独立站占跨境电商收入40.31%,亚马逊占53.76%,可学习多渠道运营;海外仓毛利率提升至15%,启示物流效率优化。

产品生产与设计需求干货

1. 人体工学系列产品营收13.37亿元,占营收55.07%,主导生产需求;新品类如电动沙发、人体工学椅销售收入占比约8%,提示产品设计多样化机会。

2. 自主品牌占比68.93%(不含海外仓),反映生产端需支持品牌化战略,提升产品竞争力。

商业机会与电商数字化启示

1. 海外仓业务营收8.51亿元,同比增长129.88%,服务778家企业,处理包裹超400万个,启示工厂可借物流数字化提升效率。

2. 跨境电商收入增长20.36%,独立站增长20.87%,提供电商渠道合作机会,推动生产端数字化转型。

行业发展趋势与客户痛点干货

1. 海外仓营收同比增长129.88%,服务企业778家,处理包裹超400万个,同比增长超120%,显示物流服务需求激增趋势;毛利率15%提升,反映效率优化。

2. 跨境电商收入同比增长20.36%,独立站增长20.87%,突显行业向多渠道发展,客户痛点包括渠道整合和物流效率。

解决方案启示

1. 乐歌自营海外仓全球布局(17个仓,48.21万平方米),提供高效物流解决方案,可借鉴以应对包裹增长挑战。

2. 新品类占比提升,结合产品多元化,启示服务商需支持客户产品创新需求。

平台需求与最新做法干货

1. 跨境电商收入中,独立站占比40.31%,亚马逊占比53.76%,显示平台生态需求;独立站收入同比增长20.87%,提供平台招商和运营管理参考。

2. 海外仓营收同比增长129.88%,服务778家企业,处理包裹增超120%,反映商业对物流平台的需求,平台可优化合作方式。

运营管理与风险规避

1. 海外仓毛利率15%提升,启示平台需加强运营效率;服务企业数量增长,提示风险规避在库存和物流管理。

2. 整体营收增长44.64%,但净利润波动,平台可学习扣非净利润增长29.95%的核心业务模式。

产业新动向与商业模式干货

1. 海外仓业务营收同比增长129.88%,全球17个自营仓服务778家企业,处理包裹超400万个,显示物流产业快速扩张新动向。

2. 自主品牌占比68.93%(不含海外仓),结合产品多元化(新品类占8%),体现“产品+服务”商业模式创新。

新问题与政策启示

1. 净利润同比下降63.86%因非经常性收入,但扣非净利润增长29.95%,突显业绩波动问题;海外仓毛利率15%提升,提供效率优化研究点。

2. 独立站和亚马逊渠道占比数据(40.31% vs 53.76%),结合增长趋势,启示政策需支持多渠道平衡发展。

返回默认