屈臣氏财报显示全球增长但中国市场疲软,需关注关键数据和转型策略。

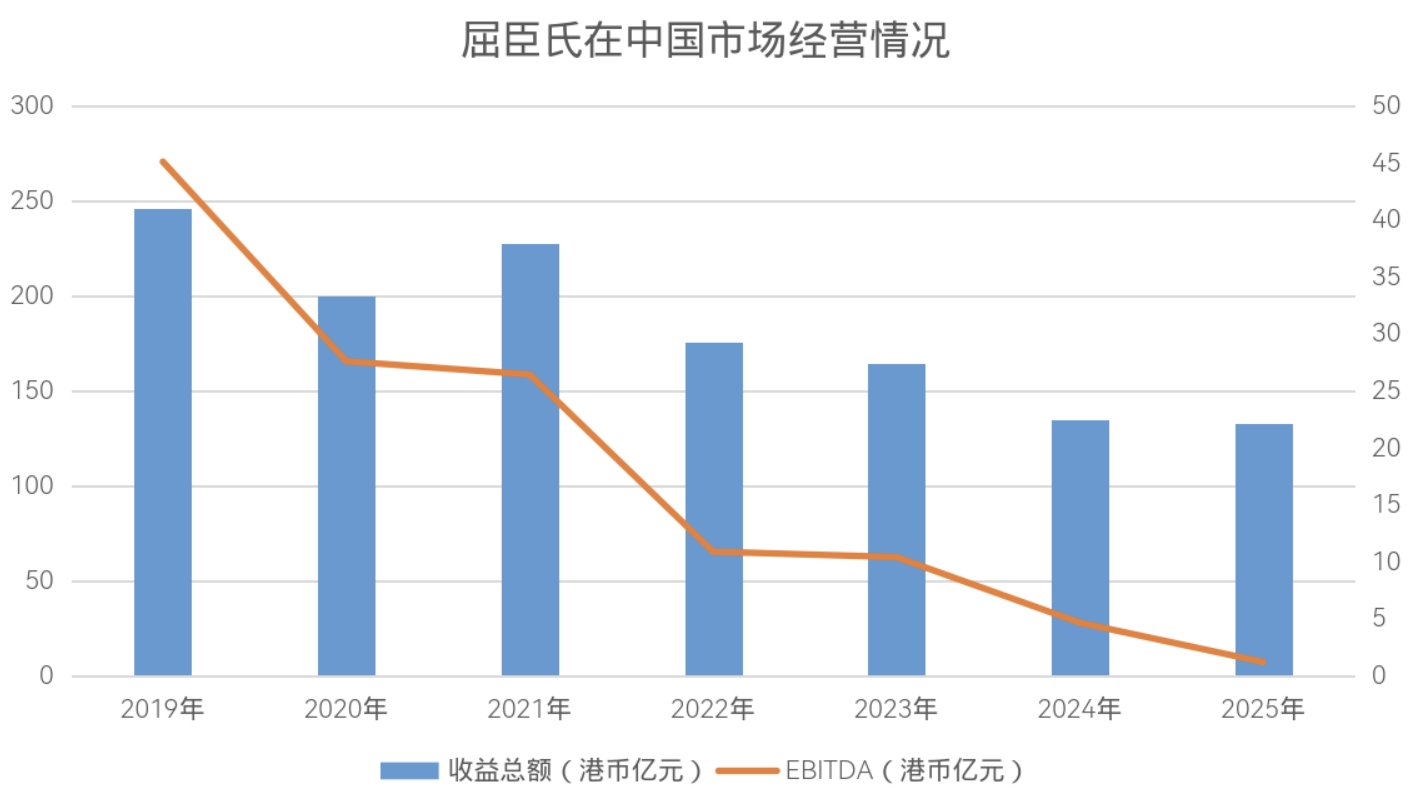

1. 全球表现:2025年营收2092.67亿港元,同比增长10.03%;EBITDA为182.38亿港元,增长11.24%;店铺总数17114家,净增294家。

2. 中国市场疲软:营收132.65亿港元,同比下降1.8%;EBITDA仅1.22亿港元,骤降73.88%;门店从3744家缩减至3465家,净关279家。

数字化转型是重点,从关店转向线上业务。

1. 幕后店加速扩张:2024年底131家,2025年中增至394家,预计年底达650至700家;计入后总门店增长6.2%至7.5%。

2. 关店优化成效:租约期满关闭人流不足店铺,营收降幅从2024年的-15.3%收窄至-1.8%。

其他干货包括薪酬改革和全球机会。

1. 薪酬改革引发问题:2025年4月实施“奖金池”制度,管理层抽成后分配,外卖订单不计个人业绩,压缩员工收入。

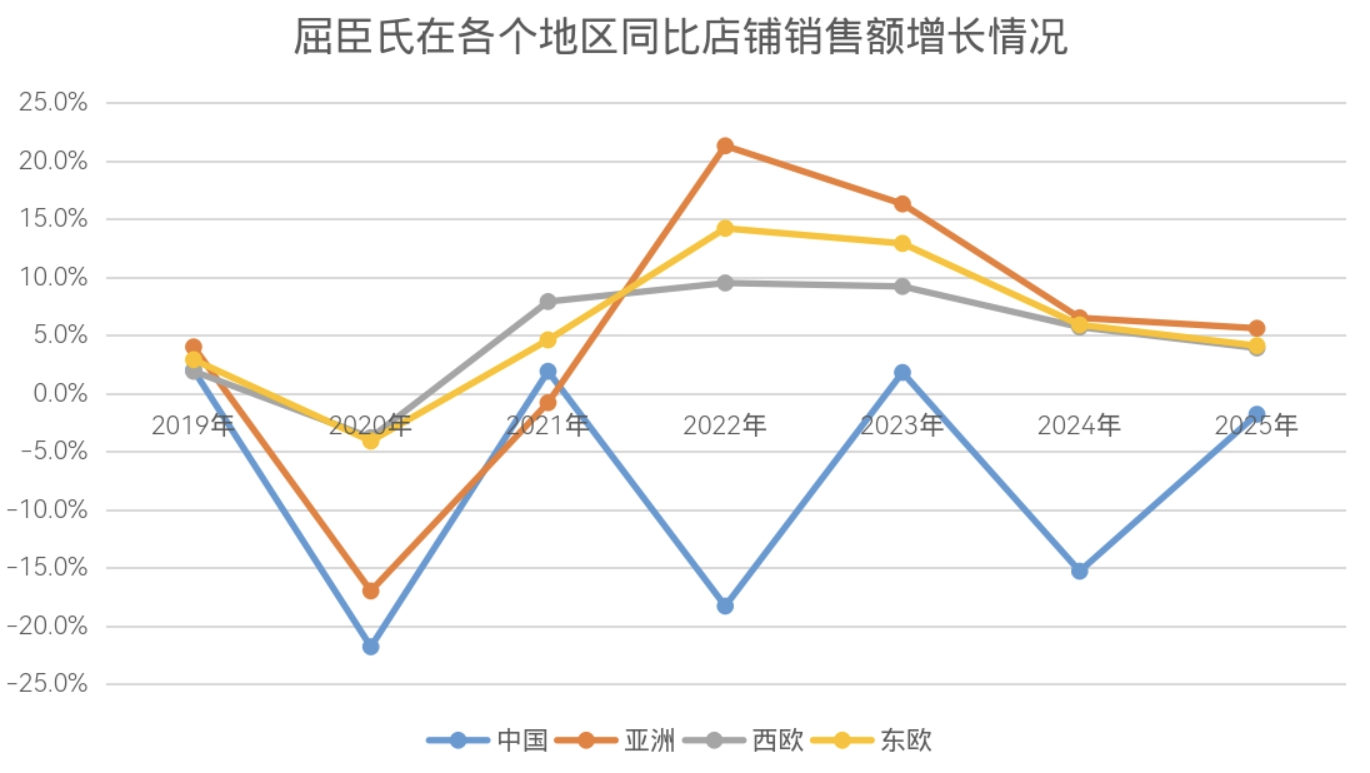

2. 全球扩张:东欧营收增长19.55%,西欧增长10.46%,亚洲增长11.54%;同店销售亚洲微降至5.6%,仍高于疫情前;IPO计划2026年上半年在香港和伦敦双重上市。

屈臣氏的财报揭示品牌营销和渠道建设策略,聚焦数字化和消费趋势。

1. 品牌渠道建设:通过幕后店加速线上业务布局,适配中国消费习惯;2025年中幕后店增至394家,预计年底700家,提升线上触达。

2. 消费趋势观察:中国消费者偏好线上购物,推动屈臣氏关店优化(租约期满关闭人流不足店铺),营收降幅收窄;会员体系稳定,忠诚会员1.81亿人,销售参与率64%。

产品研发和用户行为启示来自全球表现。

1. 全球市场差异:中国市场疲软(营收降1.8%)对比东欧增长19.55%、西欧增长10.46%,显示区域消费需求变化;亚洲同店销售5.6%,高于疫情前,反映消费回归常态。

2. 品牌营销挑战:薪酬改革(如奖金池制度)可能影响员工服务,间接波及品牌形象;线上订单不计个人业绩,提示需平衡渠道激励。

财报提供政策解读和市场机会,中国风险与全球增长并存。

1. 政策与事件应对:屈臣氏关店源于租约期满优化门店组合,营收降幅收窄;EBITDA骤降73.88%可能与转型成本相关,公司采取降本措施如薪酬改革。

2. 增长市场和机会:东欧市场营收增长19.55%,西欧增长10.46%,亚洲增长11.54%,提供扩张机会;全球门店净增294家,弥补中国关店缺口。

风险提示和学习点来自数字化转型。

1. 风险提示:中国市场疲软(营收降1.8%)和EBITDA下滑,显示经营风险;薪酬改革引发员工不满,可能影响服务。

2. 可学习点和商业模式:幕后店加速线上业务,半年内从131家增至394家,可借鉴线上渠道建设;会员体系驱动销售,参与率64%稳定。

合作方式与扶持政策:IPO计划2026年双重上市,可能带来新合作机会;外卖平台合作(如美团)但订单不计个人业绩,提示需优化合作模式。

财报揭示数字化电商启示和商业机会,聚焦产品支持与转型。

1. 推进数字化和电商启示:屈臣氏通过幕后店支持线上业务,2025年中增至394家,预计年底700家,显示工厂需适应线上供应链需求;关店优化门店组合(租约期满关闭人流不足店铺),提示生产需灵活响应市场变化。

2. 产品生产和设计需求:基于消费趋势,中国线上业务扩张,工厂可探索轻量化或定制化产品设计;全球市场增长(如东欧营收增19.55%),提供出口机会。

商业机会来自数据与案例。

1. 数据支持:营收全球增长10.03%,但中国疲软(降1.8%),工厂可分析区域需求差异;EBITDA骤降73.88%与转型成本相关,提示控制生产成本。

2. 案例启示:薪酬改革影响员工收入,工厂需关注人力成本管理;会员体系稳定(1.81亿人),可借鉴客户忠诚度提升产品粘性。

行业趋势和客户痛点突出,屈臣氏财报提供解决方案参考。

1. 行业发展趋势:数字化加速,幕后店半年内从131家增至394家,支持线上业务;全球同店销售亚洲微降至5.6%,仍高于疫情前,显示零售回归常态。

2. 客户痛点与解决方案:人流不足店铺被关(租约期满优化),服务商可提供选址分析工具;EBITDA骤降73.88%源于转型成本,公司降本如薪酬改革,服务商可开发成本管理方案。

新技术和痛点深化分析。

1. 痛点延伸:薪酬改革(奖金池制度)引发员工不满,外卖订单不计个人业绩,显示激励系统痛点;服务商可设计绩效优化方案。

2. 解决方案案例:会员体系驱动销售,参与率64%稳定,服务商可推广忠诚度技术;全球门店净增294家,服务商可支持扩张服务。

商业对平台需求和平台做法明确,财报揭示招商与风险管理。

1. 平台需求和问题:屈臣氏与外卖平台(如美团)合作,但订单不计个人业绩,显示平台需优化业绩计算系统;线上业务依赖幕后店,平台可提供招商支持。

2. 平台最新做法:加速幕后店建设(2025年中394家),平台商可学习线上渠道整合;关店优化门店组合,平台需协助风险管理。

运营管理和风向规避。

1. 运营管理:会员体系稳定(1.81亿人,参与率64%),平台可借鉴用户运营;薪酬改革问题,提示平台需规避员工激励风险。

2. 风向规避:中国市场疲软(营收降1.8%),平台应关注区域风险;EBITDA骤降73.88%与成本相关,平台需强化成本控制工具;IPO计划2026年,可能带来新平台合作机会。

产业新动向和商业模式分析,财报揭示政策启示与新问题。

1. 产业新动向:屈臣氏全球增长但中国疲软,营收降1.8%,EBITDA骤降73.88%;数字化转型通过幕后店加速,半年内增至394家,显示零售线上化趋势。

2. 新问题与政策启示:薪酬改革(奖金池制度)引发员工不满,提示劳动政策需优化;关店源于租约期满优化门店组合,政策可支持商业租赁调整。

商业模式和案例研究。

1. 商业模式:会员体系驱动(1.81亿人,参与率64%),可研究忠诚度模型;全球扩张(东欧增长19.55%)弥补中国关店,门店净增294家,显示多元化布局。

2. 政策法规建议:EBITDA下滑与转型成本相关,公司降本措施,启示政策需鼓励数字化补贴;IPO计划2026年双重上市,可分析资本市场影响。

返回默认