这篇文章核心公布了独立机构Marketplace Pulse对TikTok Shop美区卖家生态的最新研究结论,核心干货信息如下

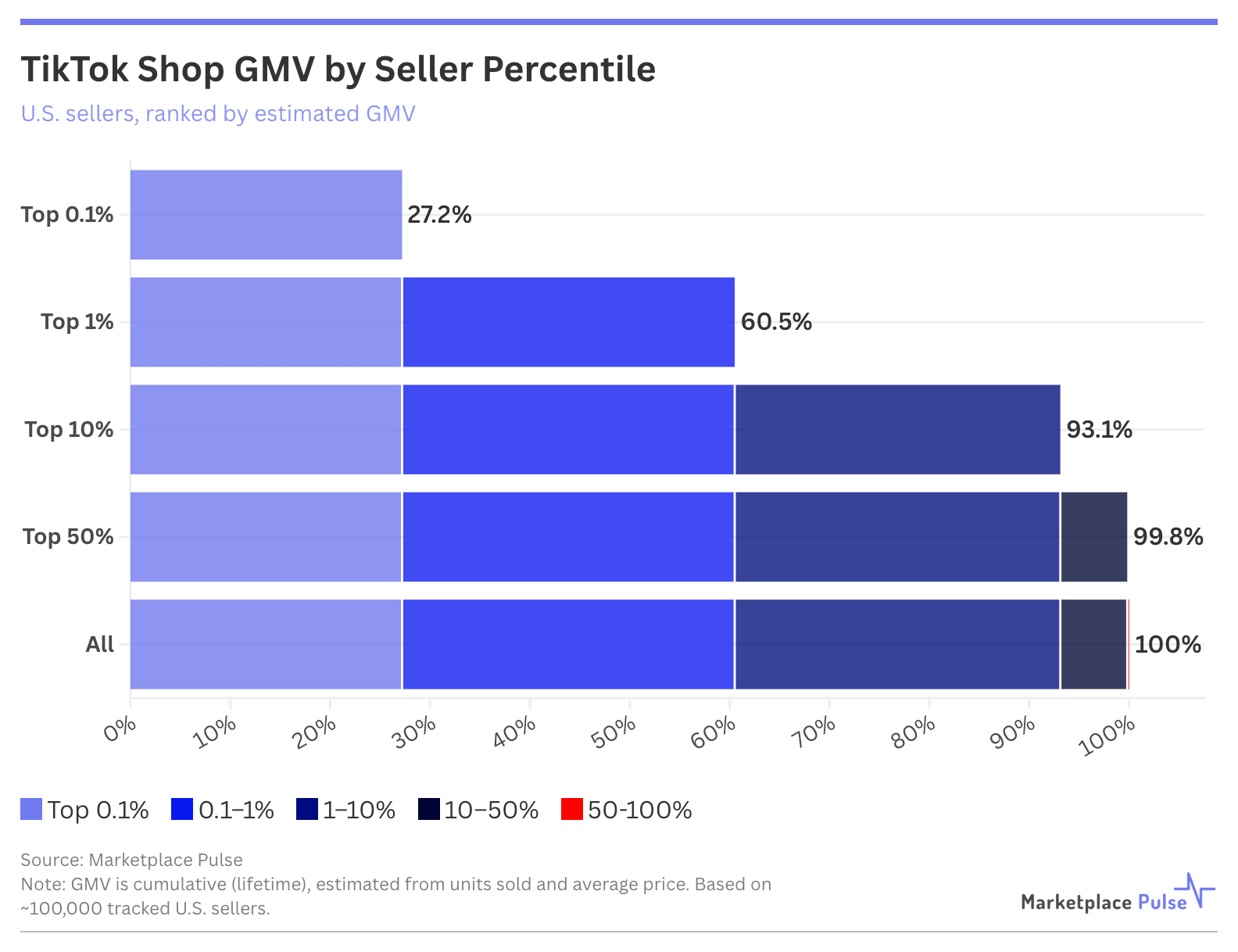

1. 核心数据显示TikTok Shop美区存在极强的顶端集中效应,研究覆盖近10万家卖家,前1%卖家不到900家,就贡献了平台60%的GMV;前0.1%卖家不足90家,平均累计销售额破1亿美元,合计贡献超25%的GMV,排名后50%卖家仅贡献0.1%GMV,头部集中度远超亚马逊。

2. 平台认证机制放大了头部效应,带有Official Store和Gold Star认证的卖家能获得更多平台曝光,官方店销售规模是未认证的40倍,金星认证卖家是普通卖家的18倍,商家规模和平台流量会形成正向循环。

3. TikTok Shop和亚马逊的竞争核心门槛不同,亚马逊决定胜负的关键是供应链管理、运营效率和资本实力,TikTok Shop的核心门槛是爆款打造能力。

本文的研究结论对品牌布局TikTok Shop美区市场有重要参考价值,核心干货整理如下

1. 当前市场格局特征明显,TikTok Shop美区头部集中程度远超亚马逊,前1%卖家掌控60%GMV,尾部中小商家份额极低,品牌入场后马太效应显著,大体量品牌拥有天然的流量优势,中小品牌突围难度较大。

2. 平台认证能为品牌带来明显的流量红利,官方认证店铺销售规模是未认证店铺的40倍,金星认证店铺是普通店铺的18倍,品牌入场后要优先拿到官方认证资质,以此获取更多曝光资源。

3. 品牌竞争方向需要调整,和亚马逊拼供应链成本、资本实力不同,TikTok Shop的核心竞争力是打造爆款的能力,品牌的产品研发和营销都需要围绕打造爆款来布局,适配平台生态特性。

对于想要入场或已经运营TikTok Shop美区的卖家,本文整理了关键参考干货如下

1. 当前格局与风险提示:TikTok Shop美区头部集中效应极强,不到900家头部卖家就占据了60%的GMV,尾部50%卖家合计仅贡献0.1%的GMV,中小新卖家入场面临极大的竞争压力,需要提前做好突围规划,不要低估竞争难度。

2. 可利用的平台机制红利:平台的官方店、金星认证会带来巨大的流量增益,卖家要优先发力获取认证资质,在获得规模增长后会进一步获得更多流量,形成正向增长循环,放大自身优势。

3. 竞争方向调整建议:和亚马逊比拼供应链、运营效率、资本不同,TikTok Shop的核心竞争门槛是打造爆款的能力,卖家要把核心资源向选品、爆款打造倾斜,避开和头部商家比拼供应链的红海。

针对想要布局跨境电商出海TikTok Shop美区的工厂,本文整理核心干货启示如下

1. 产品生产设计需求调整:TikTok Shop美区的核心竞争门槛是爆款打造能力,和亚马逊侧重供应链成本、运营效率的逻辑不同,工厂需要调整产品研发方向,更贴合海外消费热点,提升快速响应热点推出新品的能力,而非单纯走性价比走量路线。

2. 现存商业机会:目前平台长尾卖家的数据还在补充,整体头部格局虽不会根本改变,但仍给有能力的工厂留下了切入空间,工厂依托自身供应链优势,快速响应市场打造爆品,仍有机会跻身头部行列。

3. 数字化转型启示:工厂做自运营电商出海,要尽早争取平台官方认证,积累销售规模后就能获得平台更多流量倾斜,形成正向循环,推动自身的数字化电商转型,拿到出海增长红利。

针对服务跨境出海的服务商,本文整理行业相关干货如下

1. 行业发展趋势:TikTok Shop美区的头部集中速度和程度都远超传统电商亚马逊,马太效应已经初步显现,平台生态资源快速向头部商家聚集,未来服务商的核心客户结构也会逐步向大卖家、头部商家倾斜。

2. 客户痛点梳理:不同层级卖家痛点差异明显,中小卖家缺爆款打造能力,难以突破流量门槛获得增长;头部卖家需要维持爆款持续产出,巩固自身的认证和流量优势,维持头部地位。

3. 业务发展方向:服务商可以针对性开发适配不同卖家的服务,比如为中小卖家提供爆款选品、内容营销打造服务,为需要拿认证的卖家提供资质辅导、运营增长服务,抓住TikTok Shop美区增长的行业红利,拓展自身业务。

对于布局跨境电商业务的平台商,本文整理核心参考干货如下

1. 现有机制的效果:TikTok Shop当前的分层认证机制对流量分配影响极大,官方店和金星认证卖家获得的流量远多于普通卖家,推动了头部集中效应快速形成,但是也导致了平台中间层卖家规模薄弱,长尾卖家生存空间极小。

2. 需要规避的风险:如果平台过度向头部倾斜流量,会导致生态快速固化,中小卖家难以成长,长期来看会影响平台的多样性和活力,想要保持生态健康,需要调整流量分配机制,适度扶持中小卖家。

3. 差异化运营方向:TikTok Shop和亚马逊的核心竞争门槛不同,平台可以围绕打造爆款的生态特性优化卖家服务,招商阶段优先引入具备爆款打造能力的商家,巩固自身和传统电商差异化的竞争定位。

对于研究跨境电商产业的研究者,本文整理核心研究干货如下

1. 产业新动向:新兴社交电商平台TikTok Shop美区的卖家头部集中程度已经超过了传统电商亚马逊,最新研究数据显示,平台前1%卖家贡献了60%的GMV,后50%卖家仅贡献0.1%的GMV,中间卖家群体十分薄弱,这种结构和传统电商呈现出明显差异。

2. 格局形成的核心原因:平台的分层认证流量分配机制,放大了马太效应,已经做出成绩的头部卖家获得更多平台流量倾斜,进一步扩大规模,形成正向循环,这种特征和社交平台算法推荐的逻辑高度契合。

3. 产业新特征:新兴社交电商的核心竞争门槛,已经从传统电商的供应链管理、资本实力、运营效率,转变为爆款打造能力,这种差异化特征为研究社交电商的商业模式和生态逻辑提供了全新的样本。

返回默认