本文核心介绍了2026年跨境电商行业普遍存在的资金痛点,以及易达云新推出的融易卖供应链金融平台的相关干货信息,核心内容如下

1. 当前跨境出海共有三道门槛,分别是流量、合规、资金,其中资金是最容易被忽略、也最致命的门槛,是阻挡卖家规模化增长的核心原因,目前卖家普遍面临爆款抓不住、旺季备货回款错配等四种资金困局。

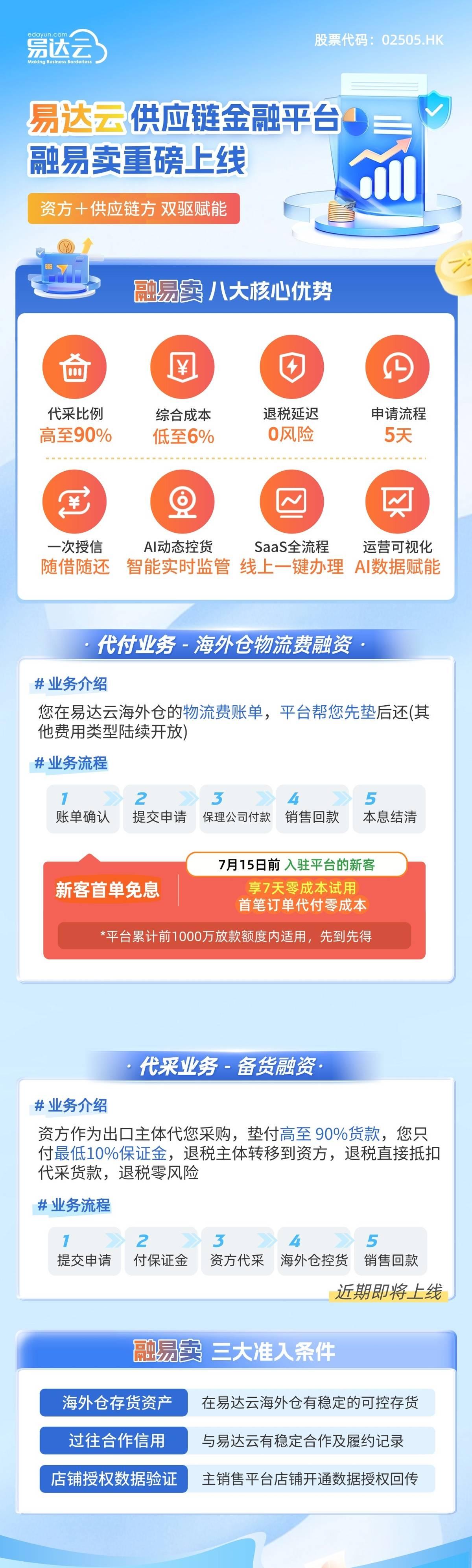

2. 融易卖是针对跨境场景打造的供应链金融平台,采用资方+供应链方双驱模式,易达云提供数据风控底座,持牌机构提供资金,核心提供代付融资、代采融资两类服务,共享授信额度,随借随还。

3. 该平台有八大核心优势,准入条件仅三条:海外仓有存货、历史信用良好、店铺数据可验证,符合条件的卖家可以抢先测算授信额度,预留资金应对未来机会。

本文揭示了2026年跨境电商出海的行业现状与增长机会,能给布局出海的品牌商提供不少参考,核心干货如下

1. 当前出海的核心门槛已经从早期的流量获取、合规适配,转向资金能力,很多优质卖家哪怕店铺数据好,也会因为资金缺口卡在规模化增长的门口,这个痛点普遍存在。

2. 行业发展趋势已经从单点能力比拼进入全链路竞争,单点能力再强,只要一个环节掉链就可能全盘皆输,品牌商可以依托成熟生态补齐非核心环节,聚焦自身品牌建设、产品研发核心能力。

3. 融易卖供应链金融可以很好解决品牌旺季备货、海外仓账单的资金缺口问题,参考年化成本仅6%-10%,低于同类服务,符合条件即可申请,能帮助品牌抓住爆款窗口,不会因为资金错过增长机会。

本文针对跨境卖家普遍面临的资金痛点推出了新的解决方案,也点明了未来行业的发展方向,干货内容如下

1. 目前跨境卖家大概率会遇到四种资金困局:爆款窗口短没钱备货错过机会、旺季备货投入大平台回款周期长、海外仓账单早于回款需要拆东补西、传统融资只看固定资产不认可跨境店铺数据,这些都是卖家经营中常见的风险。

2. 新推出的融易卖针对跨境场景设计,核心特征是不看固定资产看店铺库存数据、动态质押可边卖边融资、随借随还按天计费,能解决卖家海外仓账单压力和备货资金缺口。

3. 行业判断2026-2028年是跨境电商的分水岭,全链路效率才是竞争核心,中小卖家可以抱团依托生态平台补齐短板,符合准入条件的卖家建议先获取授信额度,等待机会来临。

本文介绍了2026年跨境电商行业的最新变化,能给对接跨境的工厂带来不少商业机会和发展启示,核心干货如下

1. 当前跨境卖家普遍面临备货资金缺口,很多卖家哪怕有优质订单,也拿不出足额现款给工厂,新推出的融易卖可以解决卖家的备货资金问题,卖家资金周转顺畅后,会给工厂带来更多更稳定的订单,工厂不用担心回款风险,可以拿到稳定的批量订单。

2. 行业趋势显示跨境已经进入全链路生态竞争,中小卖家和品牌都会把仓储、物流、金融等非核心环节交给第三方生态平台,工厂可以专注聚焦产品生产和设计,不需要额外投入资源搭建全链路,专注核心能力就能获得发展。

3. 目前卖家抓爆款的窗口只有4-8周,对排单效率要求很高,工厂需要提升自身排单响应速度,才能抓住突发的爆款订单需求,获得更多增长机会。

本文清晰梳理了当前跨境电商行业的核心痛点和未来发展方向,对跨境服务商优化服务、拓展业务有很多参考价值,干货如下

1. 当前跨境卖家的核心痛点已经从流量、合规转向资金,资金缺口已经成为阻碍卖家规模化的核心门槛,传统金融机构不懂跨境场景,无法匹配卖家基于店铺数据、库存授信的需求,市场存在大片空白,是服务商可以切入的方向。

2. 行业发展趋势是从单点能力竞争转向全链路生态竞争,单一服务已经无法满足卖家需求,生态聚合、抱团出海是未来的主流方向,服务商可以探索和不同环节玩家联合,打造整合式服务提升竞争力。

3. 融易卖的模式给行业提供了成熟参考:依托自身仓储物流SaaS积累的数据搭建风控底座,联合持牌金融机构双驱赋能,解决了跨境场景的风控和周转需求,这个模式值得同行参考借鉴。

本文揭示了当前跨境商家对平台服务的核心需求,也给出了平台生态建设的参考方向,干货内容如下

1. 当前商家对平台的需求已经从单一的仓储、物流、SaaS服务,延伸到全链路配套服务,资金服务是商家最迫切的未被满足的需求,平台补齐金融服务板块,能大幅提升商家粘性和平台整体竞争力,吸引更多优质商家入驻。

2. 融易卖的双驱模式值得平台参考:采取“持牌资方+供应链平台”的合作模式,供应链平台输出场景和数据做风控底座,资方提供资金,既解决了跨境场景的风控痛点,又匹配了商家的实际资金需求。

3. 未来跨境平台的竞争核心是全链路效率,打通仓、物流、SaaS、金融全链路的平台才能胜出,平台运营要走生态聚合路线,整合不同环节资源给商家提供完整基础设施,还可以针对符合条件的商家开放授信测算,提前挖掘优质商家。

本文记录了2026年中国跨境电商行业的最新发展变化,呈现了产业新动向和创新商业模式,对产业研究有较高参考价值,核心内容如下

1. 产业发展新动向:跨境电商的核心竞争点已经从早期的流量争夺、合规建设,逐步转向全链路效率竞争,资金门槛已经成为当前阻碍中小跨境卖家规模化增长的核心痛点,传统金融服务的授信逻辑和跨境电商轻资产、未来导向的模式不匹配,存在明显的市场空白。

2. 创新商业模式:融易卖开创了“资方+供应链方”双驱赋能的供应链金融新模式,依托供应链方多年积累的海外仓、物流、店铺运营数据搭建风控底座,解决了资金方和卖家之间的信息不对称问题,针对性推出代付、代采两类服务适配卖家不同场景的周转需求。

3. 行业层面提出了新判断:2026-2028年是跨境电商的发展分水岭,生态聚合、抱团出海是未来的主流发展方向,全链路基础设施整合会成为行业新的研究方向。

返回默认