鸣鸣很忙2025年核心业绩数据亮眼,GMV超935亿元,同比增长68.50%。

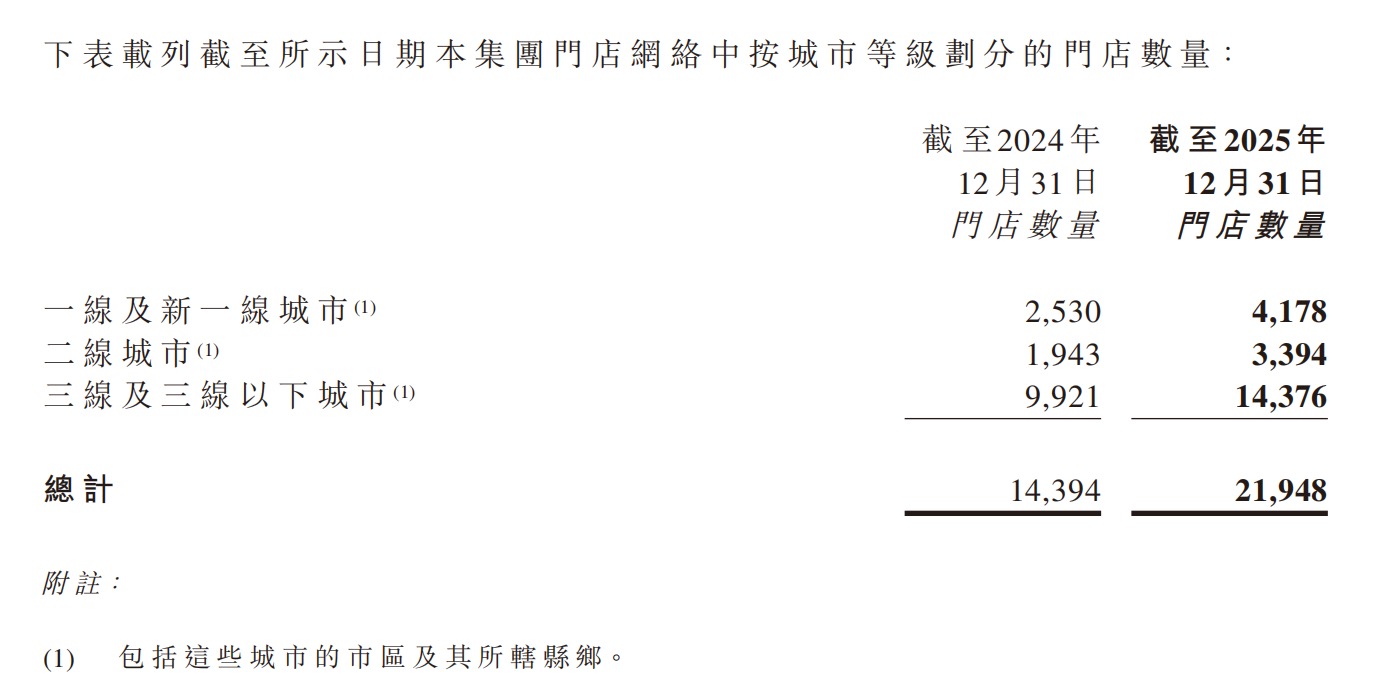

1.门店规模达21948家,覆盖30省份,下沉市场占比60%,县城覆盖率达75.0%。

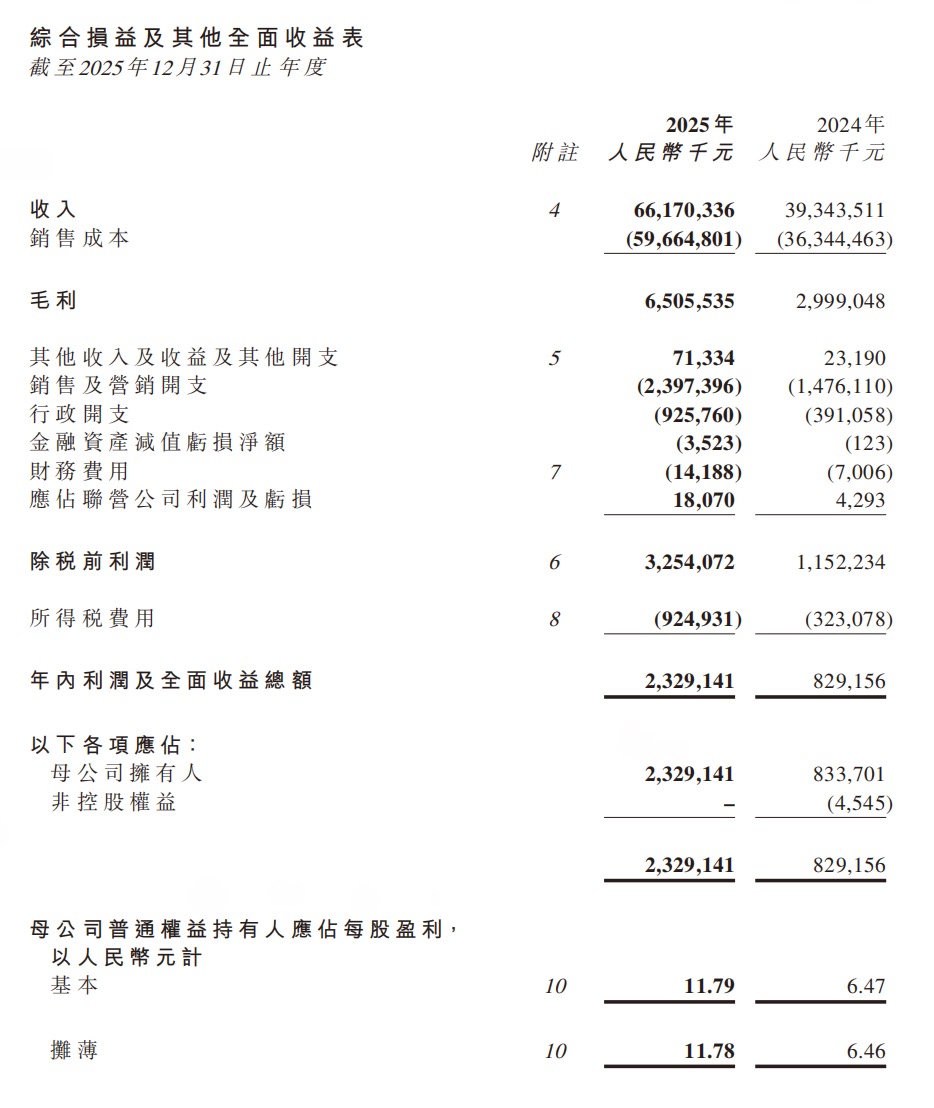

2.收入661.70亿元同比增长68.2%,利润23.29亿元增长180.89%,毛利率升至9.8%。

单店运营实操干货详尽,投资回报可靠。

1.单店投资80-100万元,现金流回本周期约2年,日均客流400-500人,客单价30元,毛利19%,净利8-10%。

2.闭店率仅1.2%,风险低,会员规模2.1亿,复购率76%,会员客单价高70-80%。

品牌营销成效显著,会员体系驱动高复购和客单价提升。

1.会员数量2.1亿,复购率达76%,会员客单价比非会员高70-80%,显示用户粘性和消费升级趋势。

2.下沉市场覆盖广,门店60%位于县城及乡镇,覆盖1401个县,反映品牌渠道下沉战略的成功。

产品研发差异化突出,主打情绪价值定位。

1.与传统零售80%商品不同,强调提供美好生活,契合消费趋势转变。

2.GMV达935.69亿元,增长68.50%,商品销售毛利好,毛利率从7.3%升至9.3%,源于规模经济和成本管控优化。

增长市场机会明确,全国量贩零食店容量超10万家,公司目标门店4-5万家。

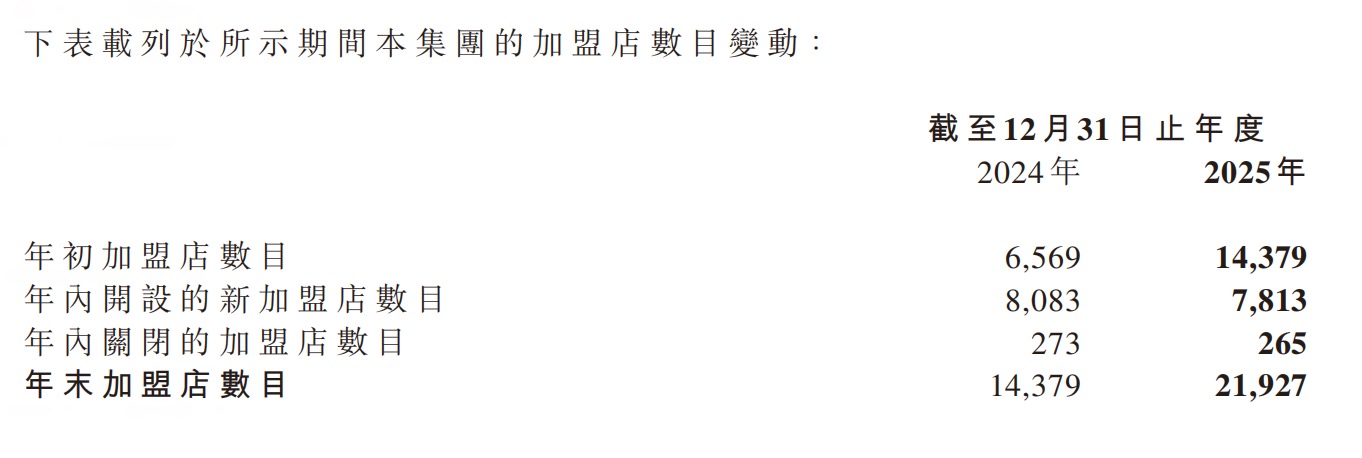

1.加盟模式为主导,99.9%为加盟店,新门店中60%来自老加盟商,40%为新加盟商,显示可持续扩张。

2.GMV同比增长68.50%,收入661.70亿元增长68.2%,市场潜力巨大。

风险与机会提示到位,单店投资回报稳健。

1.单店投资80-100万,2年回本,净利8-10%,闭店率1.2%,风险可控。

2.会员复购率76%提供需求保障,但需注意销售成本增长64.16%带来的成本压力。

商品生产和采购需求旺盛,销售成本达596.65亿元,同比增长64.16%。

1.源于向厂商采购零食饮料产品,机会大,商品销售规模656.64亿元增长67.7%。

2.商品销售毛利61.12亿元增长113.08%,毛利率升至9.3%,显示生产效率和规模经济优势。

商业机会聚焦数字化转型,成本管控强化。

1.规模经济带动毛利提升,总毛利65.06亿元增长116.92%,毛利率9.8%。

2.门店扩张至21948家,覆盖下沉市场,供应链需求增强,工厂可对接庞大采购网络。

行业发展趋势下沉市场为主,覆盖广且会员体系高效。

1.门店覆盖30省1401个县,75%县城覆盖率,60%位于县城及乡镇,代表下沉渠道扩张方向。

2.会员复购率76%和客单价提升方案,会员客单价高80%,显示用户忠诚度管理痛点已被解决。

解决方案可借鉴加盟支持体系,门店运营指标稳定。

1.加盟商10327家,新门店60%老加盟商拓展,提供客户发展模板。

2.单店日均客流400-500人,毛利19%,闭店率1.2%,运营风险管理有效。

平台招商策略完善,加盟模式占主导。

1.99.9%门店为加盟店,收入主要来自商品销售和服务费,新门店40%来自新加盟商,招商需求强劲。

2.单店投资80-100万,回本周期2年,吸引力高,GMV达935.69亿元增长68.50%。

运营管理和风向规避表现优秀。

1.单店毛利19%,净利8-10%,闭店率仅1.2%,风险低。

2.覆盖1401个县,下沉市场占比60%,平台扩张策略稳健,避免过高风险。

产业新动向突出量贩零食创新模式,主打情绪价值差异化。

1.与传统零售80%商品不同,强调提供美好生活,代表新消费趋势。

2.门店规模21948家,覆盖下沉市场,反映消费下沉和产业升级动向。

商业模式研究价值高,加盟为主收入结构清晰。

1.收入661.70亿元中,商品销售656.64亿元,服务费5.07亿元,加盟商10327家。

2.市场规模预测全国容量超10万家店,公司目标4-5万家,提供政策启示。

返回默认